For my attention challenged or just plain busy friends, if you don’t have time to read this post in its entirely then skip down to the bottom and do the 3 Actions steps.

Ask yourself; are you better off than you were four years ago?

Some 32 years ago, then presidential candidate Ronald Regan asked that question of American Voters and then walked away with the election. Clearly, many felt they were indeed worse off than they had been just four years earlier.

What if we ask the same question of your family today?

If you really want to have control over your life, you have to start believing that you have the power to shape your own future.

Unlike Regan, I’m asking about your very personal economy. We all know that both our national and the global economies have been struggling. High unemployment, shaky markets and the housing crash have hurt many families; however other families have fared remarkably well. Still others took a big hit but have since turned things around and are well on the road to recovery. While there is no denying that the world economy can and probably does affect your personal finances, your behavior affects them more.

Regularly tracking your overall financial health is one of the key habits you can develop to insure a positive answer to the “are we better off” question.

One fairly easy, reliable method for measuring your financial position over time is to periodically compute your net worth. We track ours once a month. Mint.com does a good job of tracking most of our accounts but our investment accounts don’t report, so we do our monthly net worth calculation in excel.

Others find that some other number makes a better yardstick. JD Roth over at Get Rich Slowly found that back in 2008, focusing on the one number he was trying to affect at the time (i.e. debt and then savings) was easier and more helpful then tracking his net worth; Why I don’t Track My Net Worth. I think in the early stages of wealth building, this is a perfectly acceptable alternative. The important thing here is to actually do it.

Pick some indicator of your progress with money and track it consistently.

One of the issues that stopped JD from calculating his net worth was the indecision of how to value the house. We allow Zillow through Mint to value the house. I don’t think Zillow does a great job of determining the actual fair market value of our home, but I do think it tracks fluctuations in the local market very well. For me, the actual number is not nearly as important as the trend. This same thinking applies to our net worth number. It’s the long-term trend of that number that really matters to me; not the actual number on any given day.

When you are on baby step 2 (paying off all your debt except the house) changes in your net worth are hugely significant. Each tiny increase is evidence of your discipline and hard work. Make sure you graph your net worth month to month and put it where you can see it easily. You might have started with a negative net worth but just watching the line move in the right direction is validation that you are doing the right thing.

Baby steps 3, 4 and 5 are all about actively saving (1st an emergency fund, then 15% of your income towards retirement plus saving for the kids college) and in baby step six you are really going to be pounding down that mortgage debt. These actions will almost all of the time produce steady upticks in your net worth number.

Nonetheless, as the percentage of your assets held in investments increases, it is not usual to have a bad market month that really kicks your net worth in the teeth or a great month that starts you thinking if your money can make that much in a month you don’t need to work. Remember your long view here, market and real estate losses (or gains) are not realized until you sell. Calmly, plot you net worth number for the month and move on. Month by month, year by year you will be not just collecting a record of your money behaviors and outcomes but you will be in real time alerting yourself to trends you can change to ensure the future you want for your family.

Take Action

- Set an appointment with yourself monthly to calculate your net worth. I do mine the last day of each month. Use whatever means you have you have to remind yourself to complete this task. I use a Google calendar event with an email reminder. You might use an iPhone reminder or a note on your paper calendar. We all need an accountability partner to ensure it gets done.

- Enter the value of your assets and liabilities in a spreadsheet like this one. First, make a copy or download the spreadsheet then customize it so it clearly lists your assets- the House, the 1999 Toyota Camry, IRA etc. and your liabilities Chase Credit Card, Home Equity loan etc. DO NOT use an online calculator; you need to keep this data. I do list vehicles and my high value boat on our statement but not personal property (furniture, clothes, jewelry). If you have high-value jewelry or collectibles that are readily convertible to cash list them at their true current market value.

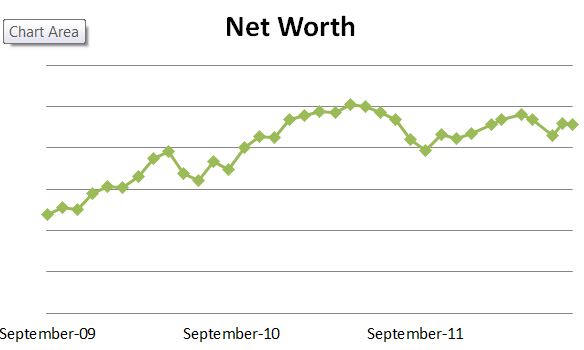

- Save your entries and plot your chart every month. Here’s mine.